Rent or Buy: Which is the Better Option in a Hot Housing Market?

The current development in the housing market makes us want to review our analysis of buying or renting a home. In a hot housing market like what we have now, is it better to rent or buy?

As a Las Vegas property management and Henderson property management company that specializes in Las Vegas luxury real estate, we checked the financial feasibility of owning a home versus renting considering data available in the market.

Owning or Renting: What is the Wiser Option?

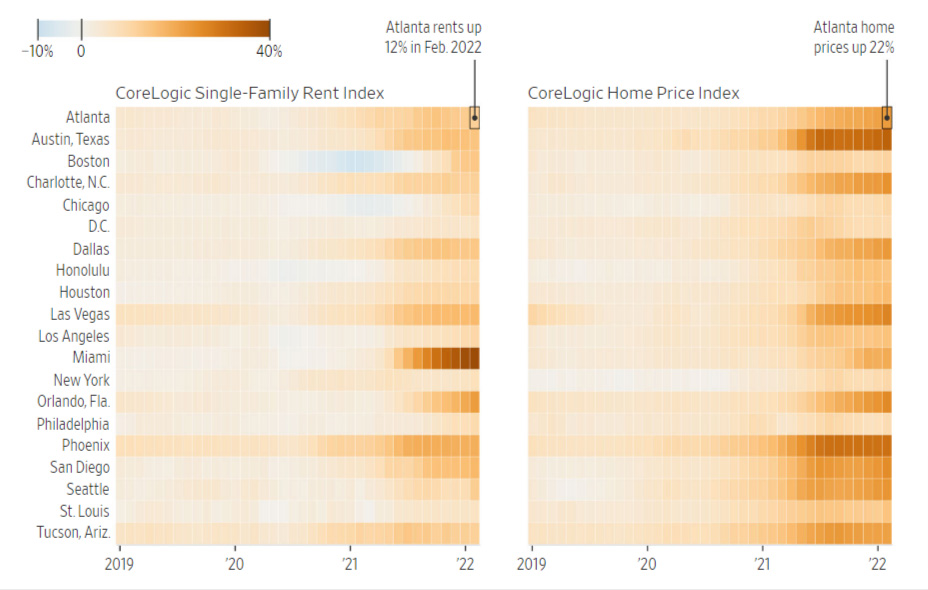

Housing data company CoreLogic compared the change in rent and home prices from last year for 20 major housing markets in the United States. It came up with the following data presented in graphical form.

Table 1. Rent and home prices, change from a year earlier (New York rent data includes Manhattan). Source: CoreLogic

Change in Rent and Home Prices

According to CoreLogic, rent for a single-family home increased13.1% in February this year, compared with the same month last year. On the other hand, home-sales prices rose even more; they were up 20.9% in March compared with a year ago.

It cited a typical example in Atlanta where rents went up 12% in February 2022. The same chart shows Atlanta home prices were up 22% from a year earlier.

Las Vegas rents were up 11% in February 2022 compared with February 2021 and home prices in the city were up 21% from a year ago.

As rising costs of owning a home make it harder for people to save for a down payment, the increase in demand for home rentals all over the country can be expected to continue, including those for single-family homes.

The hot real estate market is being driven by very aggressive demand for homes coupled with inadequate supply. The strong price growth and sales volume are expected to persist this year.

According to Freddie Mac, a secondary market financing company, interest rates have also risen. For 30-year fixed-rate mortgages, interest rates have increased to an average of 5.27% this May, up from 2.96% a year ago.

Home Purchase Break-Even Time: Pre-Pandemic Vs. Now

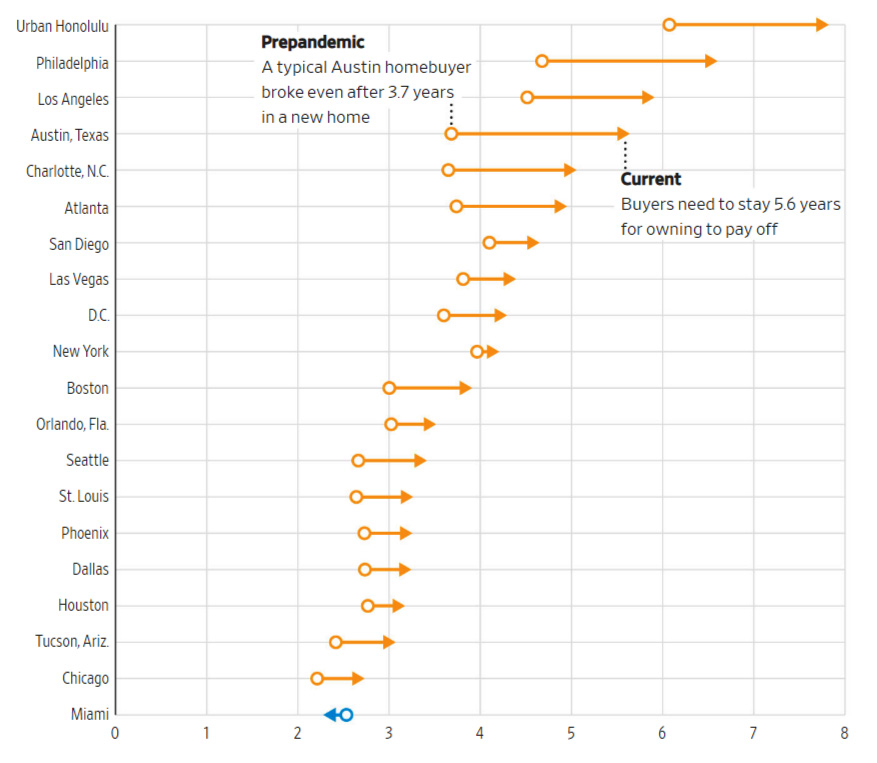

Tomo, a mortgage-finance startup, calculated the time it takes to break even on a median-price home purchase before the pandemic versus now for 20 major states in the US. The data is presented in the following chart:

Table 2. Years it takes to break even on a median-price home purchase, before the pandemic vs. now (Estimates compare December 2019 to December 2022, the most recent data available. Assumes constant down payments, loan terms, mortgage rates, and other factors across both periods to isolate for the effect of rent and home-price growth). Source: Tomo

In its analysis of rent and home-buying cost estimates from Tomo, Wall Street Journal concluded that in the current market, home buyers will have to wait longer for their investments to pay off than they would have before the pandemic. The time it takes to break even when buying a home compared with what you would pay to rent a comparable house has gotten longer. As used in this analysis, break-even is the time when the estimated net costs of having owned that home match the estimated costs of having rented a typical home over the same period.

In 19 out of the 20 housing markets covered by the CoreLogic Single-Family Rent Index, the markets used for the Tomo and WSJ analysis, the calculated time to break even on a home purchase has increased.

Austin, Texas, for example, is a market with a large increase in the time it takes to break even in buying a home. During the prepandemic, a typical Austin TX homebuyer of a median-priced home putting 10% cash down would break even after 3.7 years in a new home. Now the owner needs to stay 5.6 years for owning the home to pay off, an increase of 1.9 years.

Philadelphia is another market with the largest increase in the time it takes to break even – from 4.7 years during the prepandemic to 6.6 years now.

New York is one of the least affected by the searing home market. The break-even period in owning a home compared to renting a comparable property increased from 4.0 years to 4.2 years.

Miami is an outlier market where asking rents have risen faster than home prices. It will take less time to break even. From 2.5 years before the pandemic, it will be 2.3 years now.

For Las Vegas, the time it takes to break even on the upfront cost of buying a home, after which owning becomes a better financial option than renting has increased from 3.7 years to 4.4 years.

Benefit of Buying Instead of Renting in Terms of Cumulative Cost

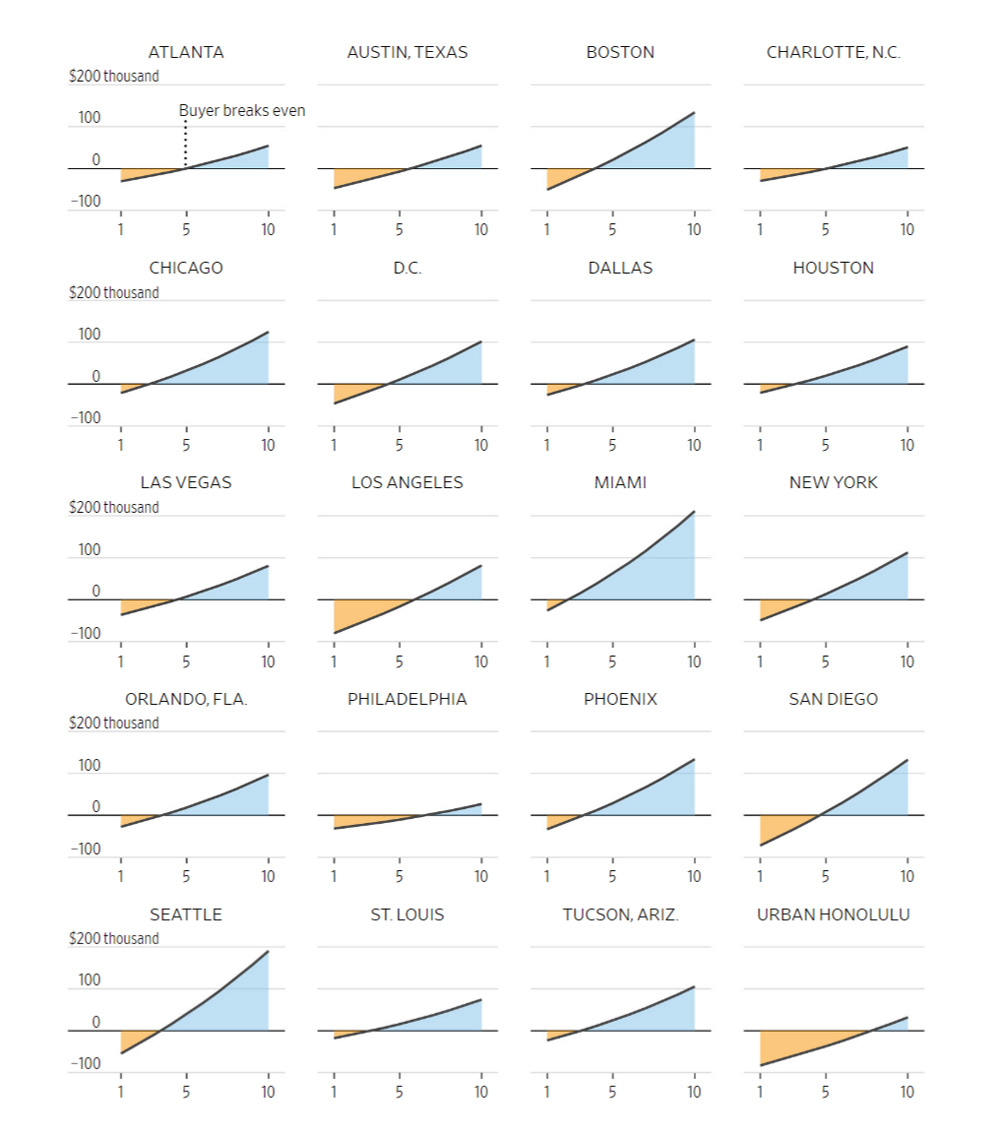

Tomo also analyzed the cumulative cost or benefit of buying instead of renting showing the first 10 years of a 30-year mortgage on a median-price home.

Table 3. Cumulative cost or benefit of buying instead of renting, first 10 years of a 30-year mortgage on a medium-price home (Accounts for estimated initial and recurring owning and renting expenses as well as projected home-price appreciation and investment returning on money renters saved by choosing not to buy). Source: Tomo

Tomo’s model shows that home buyers who sell too early stand to lose. Using Austin’s medium-priced home as a reference, it shows that an Austin home buyer who sells after just three years would lose substantially – $30,000 relative to renting a comparable home for the same period. These losses will come from the projected costs of ownership that include property taxes and maintenance, which are projected to exceed home price appreciation and the cost of renting a home with a median price over the same period.

After the breakeven point, however, the Austin buyer at the time of sale would earn up to $30,000 after eight years of owning compared with renting. After 10 years, the potential earnings would be $55,000 and after 15 years, it would be nearly $140,000.

Of the 20 major housing markets analyzed by Tomo, Urban Honolulu, Hawaii and Los Angeles are the worst-performing. The home buyers in these cities would have lost almost $100,000when selling the home after seven years and six years of owning the property, respectively relative to renting.

Miami buyers need only 2.3 years on average to achieve break-even. Financial benefits to them if they sell the property start immediately after this period. They will have a potential earning of $100,000 when the home is sold after seven years and $200,000 when sold after 10 years.

It could also be seen from the model that the Las Vegas home buyer stands to lose about $10,000 when selling after just three years compared to renting a similar home. When the break-even period has been exceeded, the seller who sells the home 8 years after it was purchased is projected to earn about $40,000. The buyer will have a potential earning of about $70,000 when the home is sold 10 years after the purchase.

In coming up with the projected outcomes, Tomo and WSJ made some assumptions in their analysis, which include the following:

- Annual rents and home-price growth will return to historical levels as they cool from their scorching, double-digit performance.

- 10% down payment was used, which is typical of its clients according to Tomo. This is however higher than most first-time buyers expect to pay especially when they avail of the Federal Housing Administration financing allowing down payments as low as 3.5%.

- Renters make investments in the stock market if they opt not to buy a home.

If the mortgage interest rates continue to rise this year, the break-even timelines could even be longer. Some families might stretch their household budget too thin and may not afford to be homeowners.

Rick Sharga, executive vice president of market intelligence at housing research company Attom Data Solutions, which has analyzed rent-versus-buy scenarios across dozens of housing markets described what could be a typical precarious situation among households.

According to him, homeowners that plan to allocate 40% of their monthly income into home payments at a time we have 8.5 % inflation are one water heater away from missing a mortgage payment.

Some people become strongly motivated to look for a home to buy soon, upset with a high increase in rent. One of them is Firdausi Yusuf, a fashion and web designer who moved to Austin with her husband last year. A 30% increase was imposed on their rent this past fall. She’s now on a furious hunt for their own home to buy.

Concluding whether renting or owning a home today is better depends on the individual’s personal situation. Financial capacity is a big factor when deciding whether to rent or buy a house. What we presented in this article is the financial aspect of these two decision options. It is also wise to consider other factors such as your lifestyle and personal goals. Weigh out the costs and benefits of each of these factors on your income, savings, and lifestyle.

Las Vegas Property Management

If you are looking at buying a luxury home, we can help you. We are a Las Vegas and Henderson property management company that specializes in Las Vegas luxury real estate and other properties within the United States. Our listings consist of some of the best Las Vegas real estate and other properties in the most sought-after neighborhoods in the country.

We can guide you with making an intelligent buy or rent decision. Contact us to find out how we can help with your acquisition of top-of-the-line, best value luxury real estate and Las Vegas property management and Henderson property management needs.